Engaging for Responsible

Rural Finance

Acting Global, Impacting Local

Empowering People

Learn more

NEPAL

Making Agricultural and MSME Finance Work

Learn more

How businesses can improve their performance through smart use of digital technology

Learn more

DIGITAL

TRANSFORMATION

SERBIA

Development of Financial System in Rural Areas

Learn more

ARMENIA

Financing the Agriculture Sector in Armenia

Learn more

Who we are

We are a management consulting company. We build client-centric, data-driven, and innovative solutions.

What we do

We offer financial consultancy to banks and microfinance institutions in emerging markets.

Why we do it

We strive to allow both the institutions we work with and their clients to flourish.

Agricultural and rural development are essential for most emerging economies. BFC works closely with lenders to ensure adequate financing is available for this sector to develop.

With a growing global awareness of the effects of climate change on the planet, the need for green finance has become more prominent. BFC is committed to supporting those who want to develop in an environmentally responsible way.

SME financial needs require a greater degree of flexibility on the part of lenders. BFC works to develop comprehensive and flexible product packages tailored to suit each client group’s financial needs.

Microfinance allows any individual or microbusiness that lacks access to conventional banking, the ability to gain affordable financial services. BFC has extensive experience in helping lenders support this significant sector.

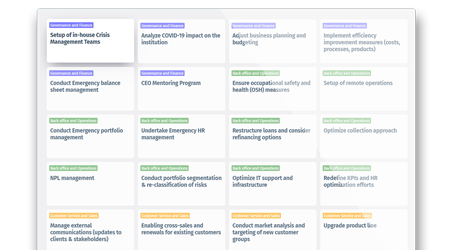

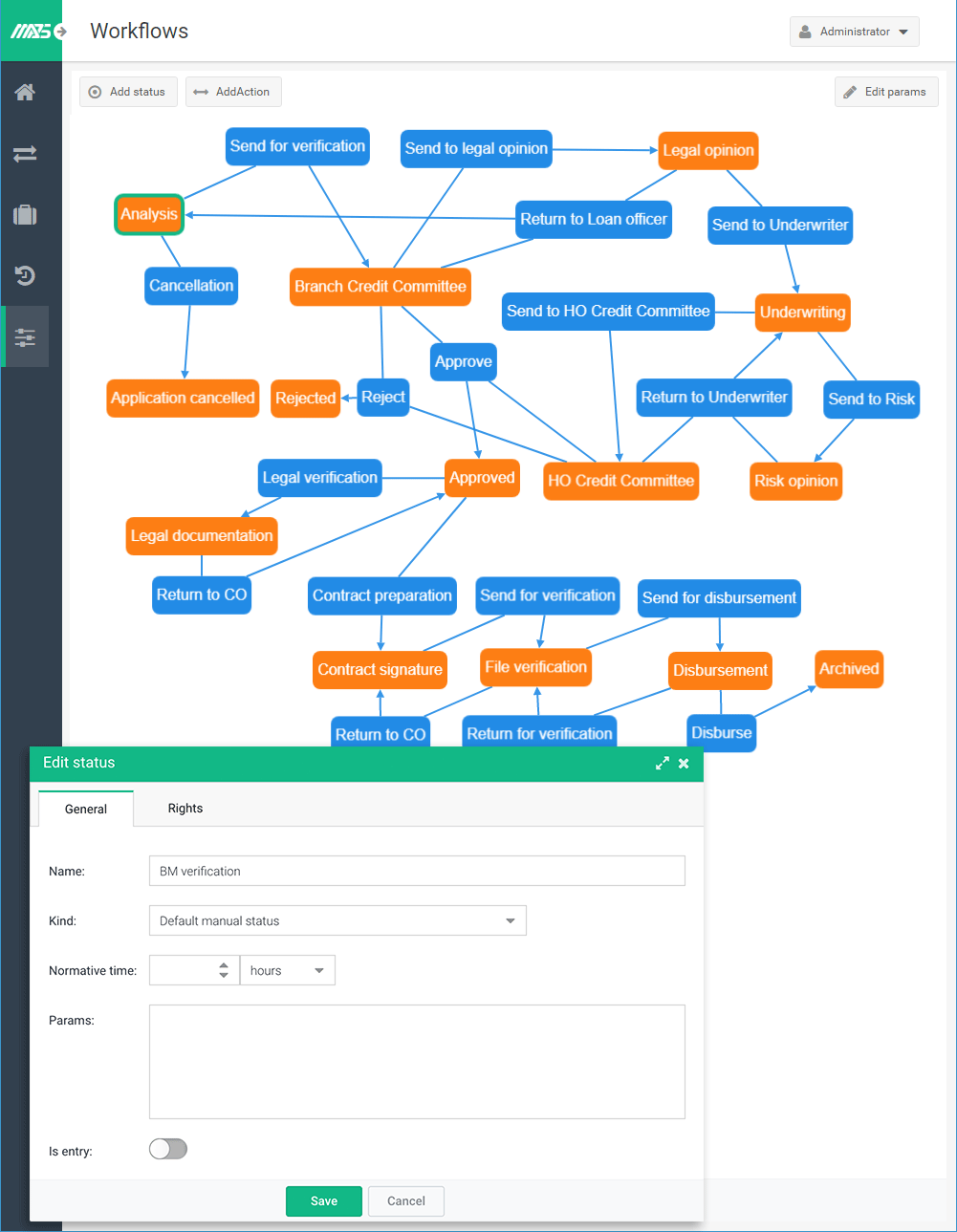

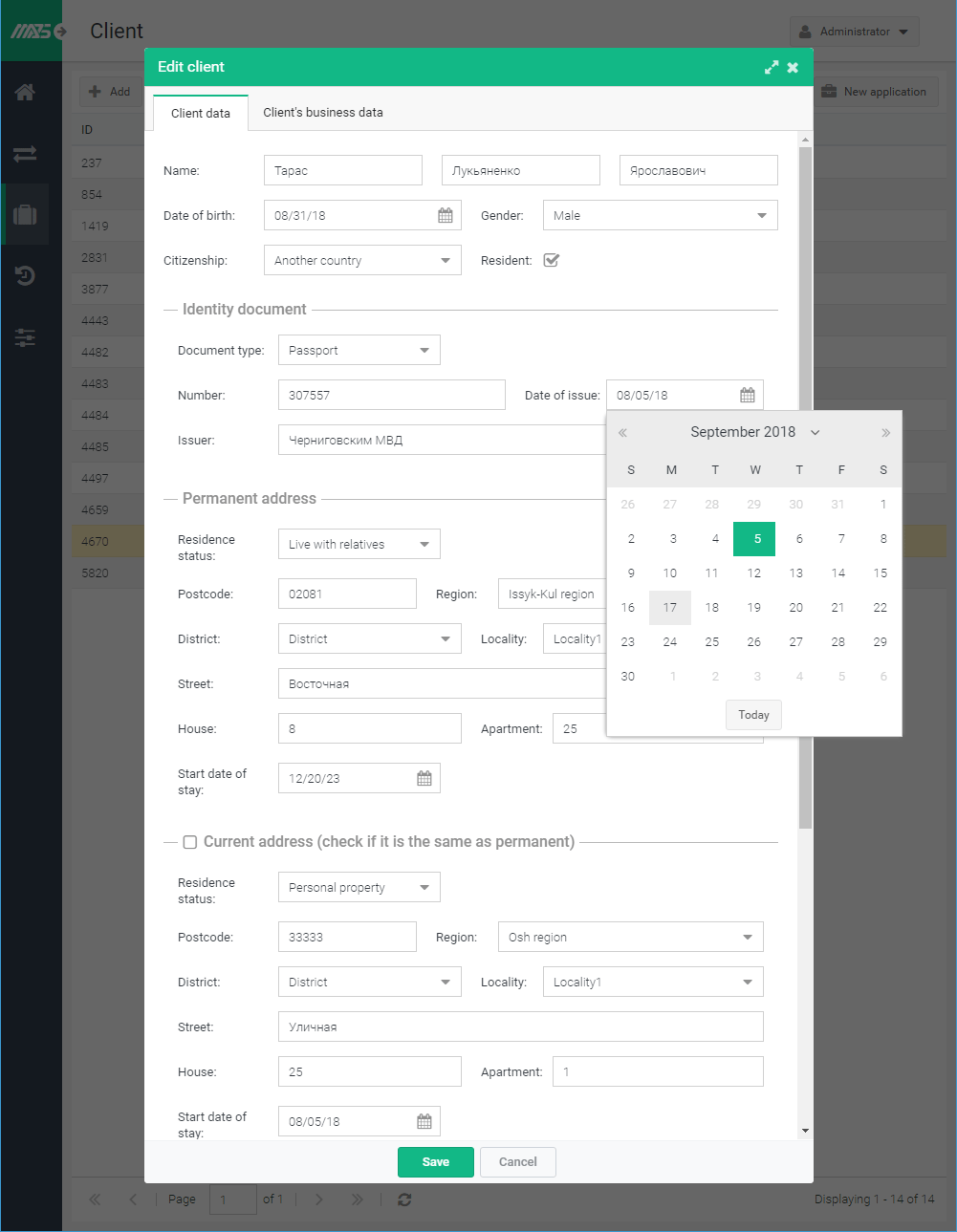

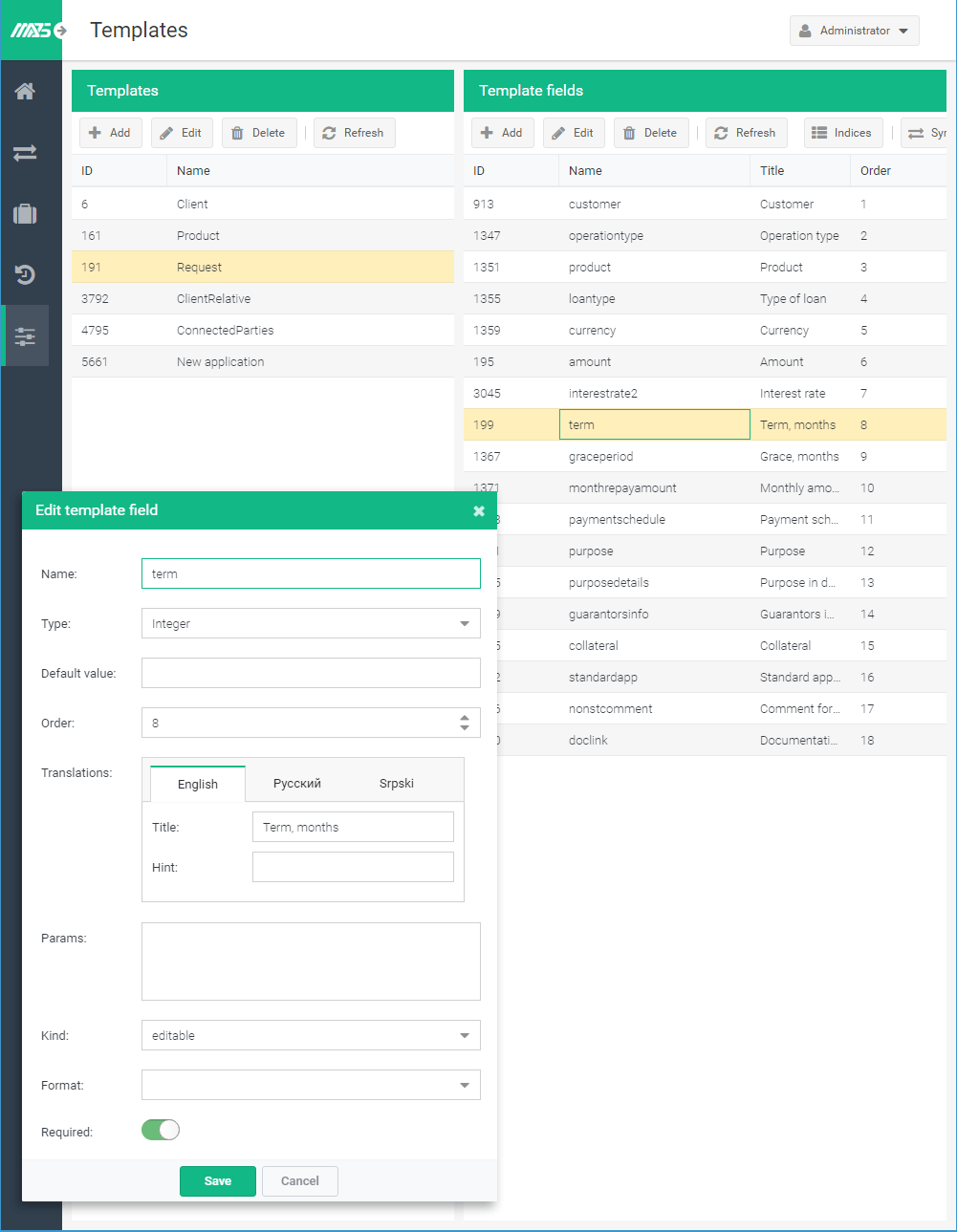

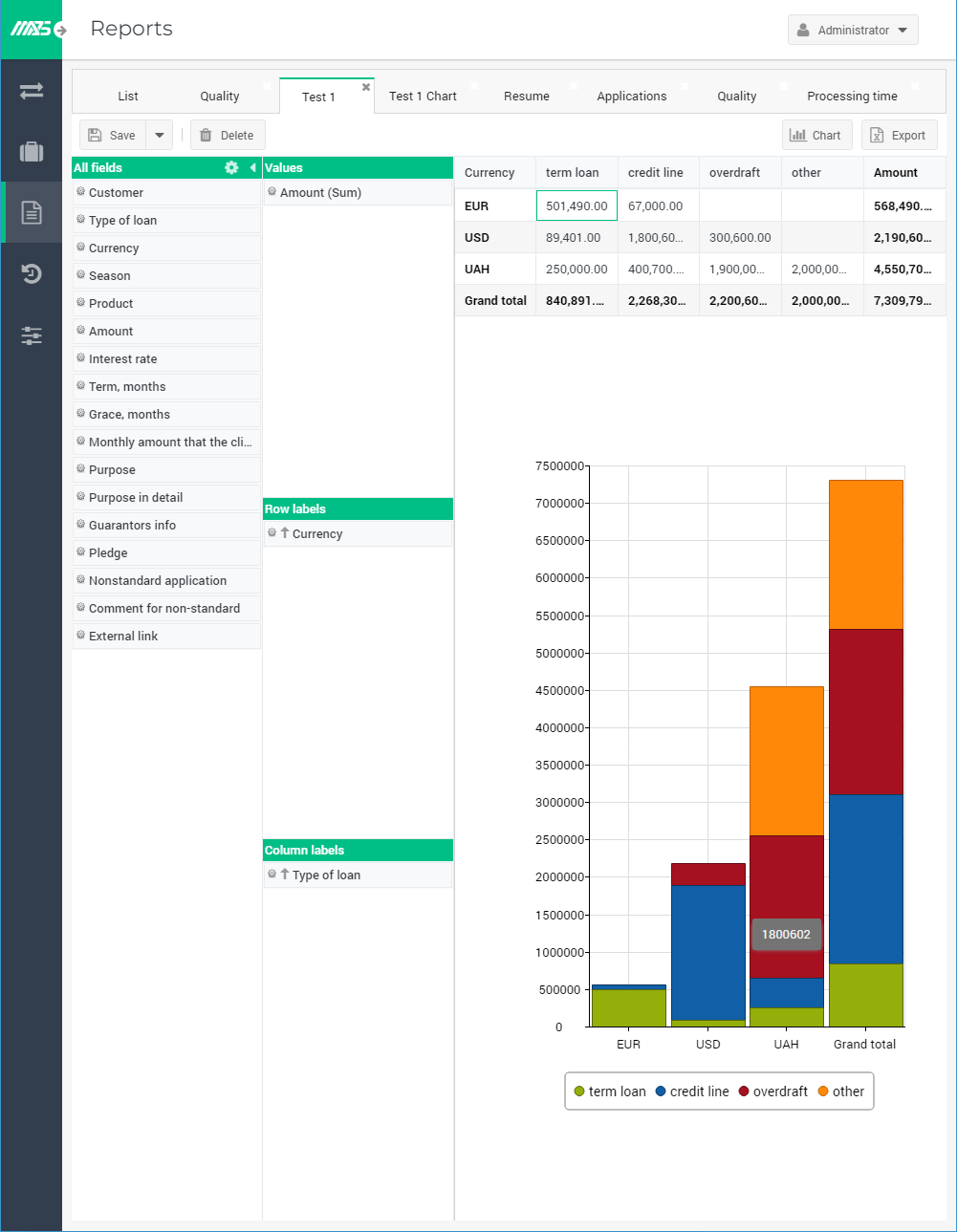

MasterAPS is a secure Application Processing System (APS) that is fully-customisable to your data and team needs. With advanced data management, easy reporting and extensive connectivity, loan processing has never been easier.

Make your credit process smarter

Securely analyse and store client data

Get all the information needed to make the right loan approval decisions

")

Upskills for Sustainable Finance")